You can't retain a 42-year-old with a ping-pong table

60% of UK workers now rank private health insurance as their most valued workplace benefit, ahead of extra holiday (41%) and life insurance (37%). That is a MyHealthPal analysis published this month, and it is a ranking that would have been unthinkable five years ago. The number also happens to be one that most benefits teams have not yet priced in.

For a century, holiday was the axis of benefits. The thing employees compared between offers. The lever HR could flex when base salary was stuck. The emotional image on the recruitment page. That axis has quietly rotated. The new axis is not how much time the job gives back. It is how much life the job adds. This is the new front in the war for talent.

Three signals the centre of gravity has already moved

The C-suite is already a step ahead of its own benefits department. The people approving your 2026 perks stack are quietly buying their own parallel one: quarterly hormone panels, NAD+ and regenerative protocols, AI-powered monitoring, executive-tier longevity programmes. Ask any senior HR leader what their CEO actually spends on personal healthcare in a year ; then ask which line item in the staff plan maps to that.

The high street is selling it as status. Life Time is rolling VO₂ max and metabolic testing into mass-market gym memberships. Luxury grocers are selling "wellness" as a visible goods-and-services category, not a lifestyle. Amex Platinum and Chase Sapphire Reserve now bundle Oura and Whoop subsidies as premium-card perks ; the category they compete on has shifted from airport lounges to health data. Whoop just raised $575M at a $10 billion valuation with LeBron James and Cristiano Ronaldo among the investors, and Oura has just been named the official wearable of U.S. Soccer. A thing is only named "official" once it has already become infrastructure.

The people you are trying to hire are already self-navigators. The 28-year-old joining your team walked in with a wrist tracker, a ring, a CGM or a biomarker subscription, and an AI tool that interprets all of it. The 42-year-old you are trying to retain has quietly spent two years buying access to the same stack in fragments. They did not do this because HR asked. They did it because it felt obvious.

The structural problem nobody in HR wants to own

Most employer health plans pay for treatment after someone gets sick. The new benefits ask is to pay for not getting sick in the first place. That is not an edit to the existing product ; it is a different product.

Two pressures are hitting this transition at the same time, and they work against each other.

Pressure one, from the CFO. Mercer's latest reporting has US employer healthcare costs rising 6.7% this year, a 15-year high. GLP-1 coverage alone is stretching budgets so hard that Medicare is pulling back and multiple plans are tightening eligibility. Finance's instinct is to spend less on health, not more.

Pressure two, from the workforce. A 2026 AJMC survey found two in three employed adults would be more likely to use GLP-1 weight-loss drugs if their employer funded them. Two-thirds of your current and future employees asking your plan to cover a preventive category that did not exist in any serious form three years ago.

The CFO sees cost inflation on yesterday's product. The workforce is asking for a newer one. HR is being asked to square that circle without a redesign budget.

Two eras of benefits, side by side

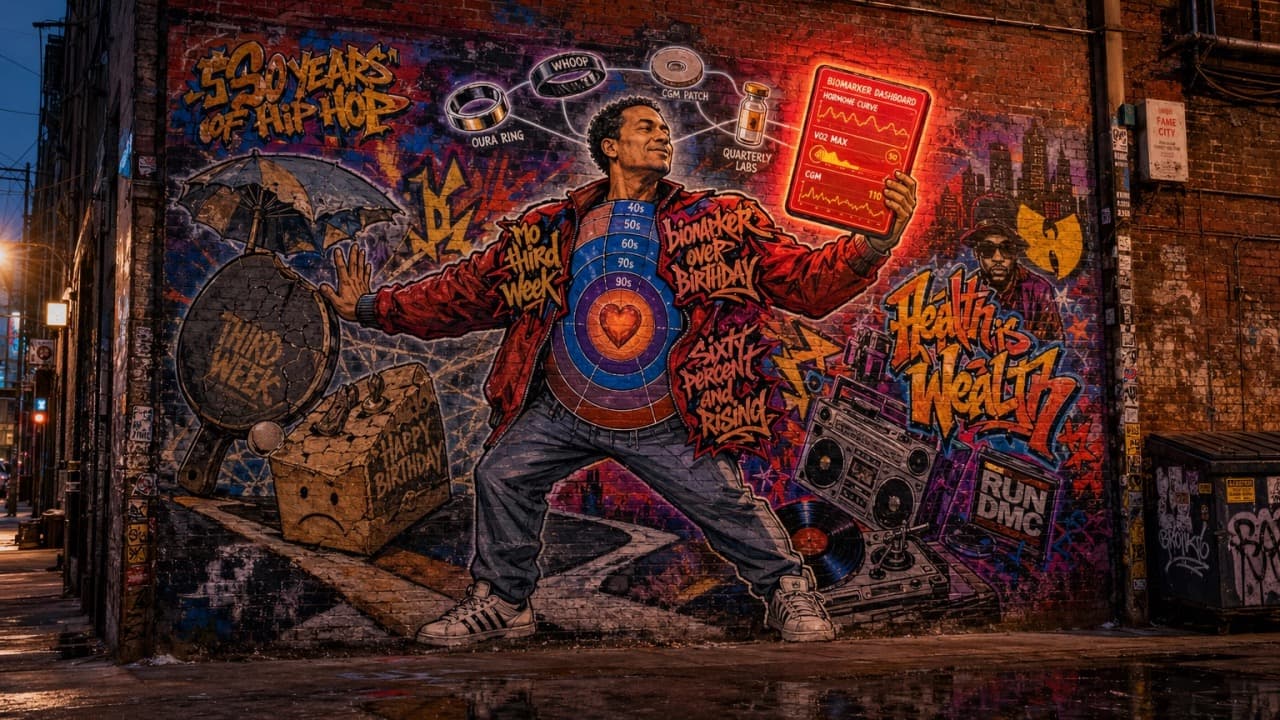

| Holiday-era benefit | Healthspan-era equivalent |

|---|---|

| Third week of annual leave | Quarterly metabolic and hormone panel |

| Gym reimbursement | Longevity or functional-medicine clinic membership |

| EAP hotline | Embedded health coach plus biomarker dashboard |

| Birthday off | Annual executive-tier health programme |

| Free snacks in the office | Food-as-medicine stipend or curated supplement allowance |

| Pension match | Healthspan match ; employer co-funds the personal longevity stack |

You do not have to agree that every row on the right belongs in your 2027 plan. You do have to notice that the right column is the one your best hires already compare you against, whether you offer it or not.

The two-tier trap inside the transition

If only the C-suite gets the longevity stack, you have rebuilt the old class divide inside the office with new language. The serious companies will flatten it. The rest will pretend it does not exist, until their top quartile of talent quietly moves to the one that did.

A useful frame from last week's Fortune piece on the longevity revolution: most of us can now expect to live into our eighties, nineties and beyond, yet our systems (insurance, Medicare, financial planning, benefits) still design for short lives and early retirement. That design lag sits inside your benefits plan too.

The forecast, layered

By 2027 ; the first Fortune 500 employer publicly swaps a week of PTO for a subsidised longevity clinic membership and frames it as a retention win. A second follows within the quarter.

By 2028 ; benefits brokers start listing "longevity stack" alongside "dental and vision" in their side-by-side comparison matrices. The phrase stops sounding Silicon Valley.

By 2030 ; a "healthspan match" line item (employer co-funding a portion of a personal longevity stack) appears in enough top-100-employer comp packages that not having one is a hiring liability at senior levels. Ten years after that, we will look back at the pension-only era the way we now look back at defined-benefit plans.

The move on Monday

Do not bolt a longevity perk onto the existing stack. That is how this gets done badly. The harder move is to audit which of your current benefits still do useful work for the people you most want to keep, and start reallocating from the ones that do not.

The first employer to offer "a longevity clinic membership and quarterly biomarker panel instead of your third week of holiday" looks absurd in 2026 and obvious in 2029. Sixty percent today. That number is not going backwards.

💥 May this inspire you to audit your own benefits stack the way your best hires already audit it ; through the lens of healthspan, not holiday.